GenesysGo: the crucial infra provider on Solana you don’t know about

Overview

GenesysGo is a blockchain infrastructure provider on the Solana network. Their three core areas of operations are (1) Shadow Operators, the RPC layer, (2) Shadow Drive, the decentralised data storage layer and (3) Shadow Cloud, a decentralised Cloud Computing platform.

In this article, we look to shed light into each of these areas before looking at the tokenomics to hypothesize the value accrual for the $SHDW token.

The growing importance of a decentralised, censorship resistant RPC Layer

The role of Shadow Operators

Remote Procedure Call (RPC) nodes act as traffic controllers which provide a means of communication between the dApps and the blockchain they are operating on. RPC nodes on Solana handle the same traffic as validators with the additional traffic of serving data lookups, which puts them under heavy load. This provides a poor user experience for users, especially for dApps utilising free RPC services.

Coupled with the reports of Infura and Alchemy restricting access to data on Tornado Cash smart contracts, the need for a fully decentralised RPC layer is stronger than ever. As of today, there are only two fully decentralised RPC providers in Pocket Network and Ankr, with the rest having centralised operations (GenesysGo included).

Despite the importance of a set of decentralised RPC nodes, there is currently no financial incentive for running one. This is where the Shadow Operators come in.

GenesysGo has built a smart contract where payments for their decentralised RPC service is paid directly to their users, in USDC. Previously, Shadow Operators were going to receive rewards in $SHDW but this change will now ensure that the Shadow Operators can pay for the operational costs that are still being denominated in fiat, without being subjected to the fluctuations of the $SHDW token.

There are currently three tiers of RPC service being provided, with a free service and two paid monthly subscriptions at $325 and $795, where 100% of the payments go to the Shadow Operators. Shadow Operators will be required to stake 10,000 $SHDW tokens as collateral, and can be subject to slashing if there is downtime, and will be required to top up their collateral in order to earn their USDC rewards.

The Shadow Operator set will remain closed to the existing 27 that have been with the GenesysGo team since the start, at least until they are economically self-sustainable with user traffic. Going forward, once there is proven demand and economics for the Shadow Operators, it will drive more people to join their RPC network, which will help with further decentralisation.

The need for a high throughput, reliable and decentralised storage

The Shadow Drive

Data on Solana today is stored in one of three ways; a) Validators and RPC, who store about a week of ledger history, b) Google big table storage or c) third party storage such as Arweave and Filecoin.

While Arweave and Filecoin are the most common third party storage solutions used, they are not compatible with Solana; the cost of storage for both is payable in their respective tokens and not SPL native, and the throughputs of both chains are unable to keep up with Solana which results in multiple failed transactions. The combination of these factors make it cumbersome for developers to integrate them on chain.

While Google Big Table can provide a reliable alternative given their large global network infrastructure, users have to rely on certain trust assumptions that data stored on Google is censorship resistant. It is also more expensive when compared to the decentralised storage alternatives.

So what is the Shadow Drive and why should it be THE decentralised data storage solution?

The Shadow Drive is an adaptation of an open source software defined storage program called Ceph, which is a great starting point due to it being:

- Open sourced; over 179 repositories, 10,000 forks and a community of tens of thousands available to provide support

- Resilient and adaptable; no singular point of failure that could lead to data loss and can be integrated with smart contracts to protect stored data against malicious intents

- Performant; cluster is so fast that a finished block can be ingested, stored and served live requests against it before the next block is propagated

- Scalable; largest cluster ever tested successfully stored 10b unique objects, making it suitable for Solana’s fast blocktimes (146m blocks at time of writing)

- Efficient mapping algorithm CRUSH; it allows for decentralisation of location for data on an individual byte level

The GenesysGo team then integrated it directly with the Proof of History mechanism, passing on-chain events for consensus approval by the Solana validator network which prove the continued existence and integrity of the stored data. Moreover, the Shadow Drive is a singular platform which provides a solution for storage, uploads and serving of the data. In comparison, Arweave utilises Bundlr for faster uploads and ArDrive for serving of the data, adding further complexity to the user experience. Read here for a more detailed explanation on the architecture of the Shadow Drive.

Overall, the Shadow Drive is cost effective and easy to access, optimised for speed and reliability to handle Solana’s throughput, altogether providing a frictionless user experience.

A decentralised cloud computing environment

The Shadow Cloud

The Shadow Cloud was recently unveiled by GenesysGo with an aim at decentralising cloud compute services and offering lower price points than what traditional, centralised business like Amazon and Microsoft does. This will be powered by a Directed Acyclic Gossip Graph Enabling Replication (DAGGER) that is built by the GenesysGo team, which serves as a L1 distributed ledger technology to handle large data structures. A Shadow Cloud Testnet environment will be up and running at the Solana breakpoint conference where developers can try it out. Not many details have been shared at the moment, and will be revealed during the conference.

Tokenomics

GenesysGo launched an NFT drop on 3 November 2021, selling 10,000 NFTs for 2.5 SOL when SOL was ~US$220. They proceeded to launch an IDO on 3 January 2022, raising c. US$52m, giving a TGE price of ~$1.73 for $SHDW.

As of 31 Oct 2022, the max supply has been readjusted to c. 170m tokens after the team decided to burn 30m of tokens from the Strategic Reserves and Operator Emissions pool. This decision was made because Shadow Operators will now receive revenues directly in USDC, rendering the Operator Emissions pool redundant, and the team no longer saw a need to have any Strategic Reserves set aside.

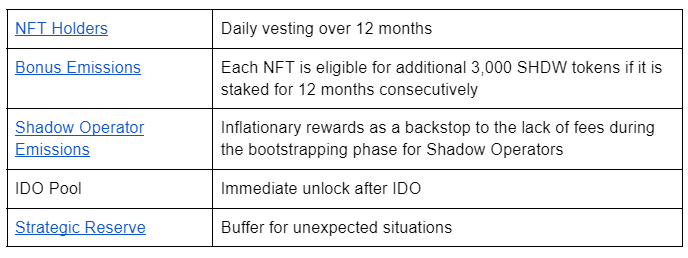

Breakdown of Token Stakeholders:

Key Highlights on Supply:

- As of 31 Oct, about 82.5m of a potential 130m tokens from the NFT holders remain in the NFT staking contract. This represents 48.5% of the total supply.

- The first full vesting for NFT emissions will be done by January 2023..

- 7m tokens under Strategic Reserves were loaned to Alameda to do market making across Serum and Orca pools. Terms of the loan are 3 years, with an option to purchase tranches of tokens at different prices (undisclosed), all priced significantly above the IDO price of $1.70.

Demand Mechanics:

Demand for $SHDW will be derived from being:

- A storage fee token for data storage on the Shadow Drive

- A form of collateral for Shadow Operator Nodes

Demand for Shadow Drive

According to Metaplex, there have been 15m NFTs minted in the past year. Assuming an average of ~50mb per image, this requires 750,000GB of decentralised storage. This allows us to establish a lower bound demand of 187,500 SHDW tokens annually, assuming immutable storage, and an upper bound of 750,000GB of SHDW locked up as storage rent assuming mutable storage.

Another strong use case is to store Solana’s historical state which grows at a rate of 4 petabytes of data (4m GB) a year. This allows us to establish a lower bound of 1,000,000 of SHDW tokens for immutable storage, and an upper bound of 4,000,000 SHDW tokens a year in storage rent for mutable storage..

Putting these 2 prominent use cases together, we can deduce that there is a potential demand of 1,187,500–4,750,000 of SHDW per annum. In other words, a potential demand of 0.69% — 2.80% of total SHDW supply per annum for storage fees to store data on the Shadow Drive.

Demand for Shadow Cloud + RPC

According to GenesysGo, there are a total of 27 live Shadow Operators today. Given the staking requirements of 10,000 SHDW to be eligible for SHDW emissions and fee sharing, we can deduce that there are 270,000 SHDW removed from circulation.

The team has also stated that they envision a network of “several thousand” Shadow Operators that could be powering the RPC network and Shadow Cloud. If we assume 1,000 Operators, that will translate to 10m SHDW locked away as collateral, reducing SHDW supply by c. 5.88%.

Pulling it Together

Overall, the economic design of the token will be driven by utility. Tokens are demanded by two sets of users: (a) people who are seeking storage solutions via Shadow Drive and (b) shadow operators who want to contribute compute resources in return for an income.

On (a), as long as Shadow Drive provides a comparable storage experience to traditional cloud storage and at a lower cost, the onus would be on the business development and education front to onboard users to the platform. With more users, the demand for storage and token would then increase.

On (b), as long as the potential income from providing compute for Shadow RPC, Shadow Cloud and potentially Shadow Drive too outweighs the costs and difficulty of operating a Shadow node, we can expect to see a greater demand for more Shadow Operators. This will then increase the amount of SHDW locked as collateral, akin to buying ASICs for mining.

On the supply side, we expect volatility to continue into Q2 2023. Beyond the remaining token vesting for the NFTs, there are no further supply vestings. At that point, the total supply will be fully circulating and will be driven by the utility mentioned above.

We will be looking out for more updates from the team at breakpoint, especially on the Shadow Cloud and what it means for the SHDW ecosystem.

Note: The information and publications are not intended to be and do not constitute financial advice, investment advice, trading advice or any other advice or recommendation.

Written By Henry Ang, Mustafa Yilham, Allen Zhao & Jermaine Wong